Following our longitudinal study of Hyperbolic Discounting: The Temporal Trap of Deferred Payments, this research explores Social Scoring Integration as a critical proxy for creditworthiness. In the 2026 financial ecosystem, institutional algorithms have moved beyond isolated balance sheets. These systems now analyze the digital associations and network proximity of an agent. This shift recognizes that financial behavior is often socially contagious. Therefore, the audit layers treat digital footprints as valid indicators of systemic reliability.

Social Scoring Integration and Network Mechanics

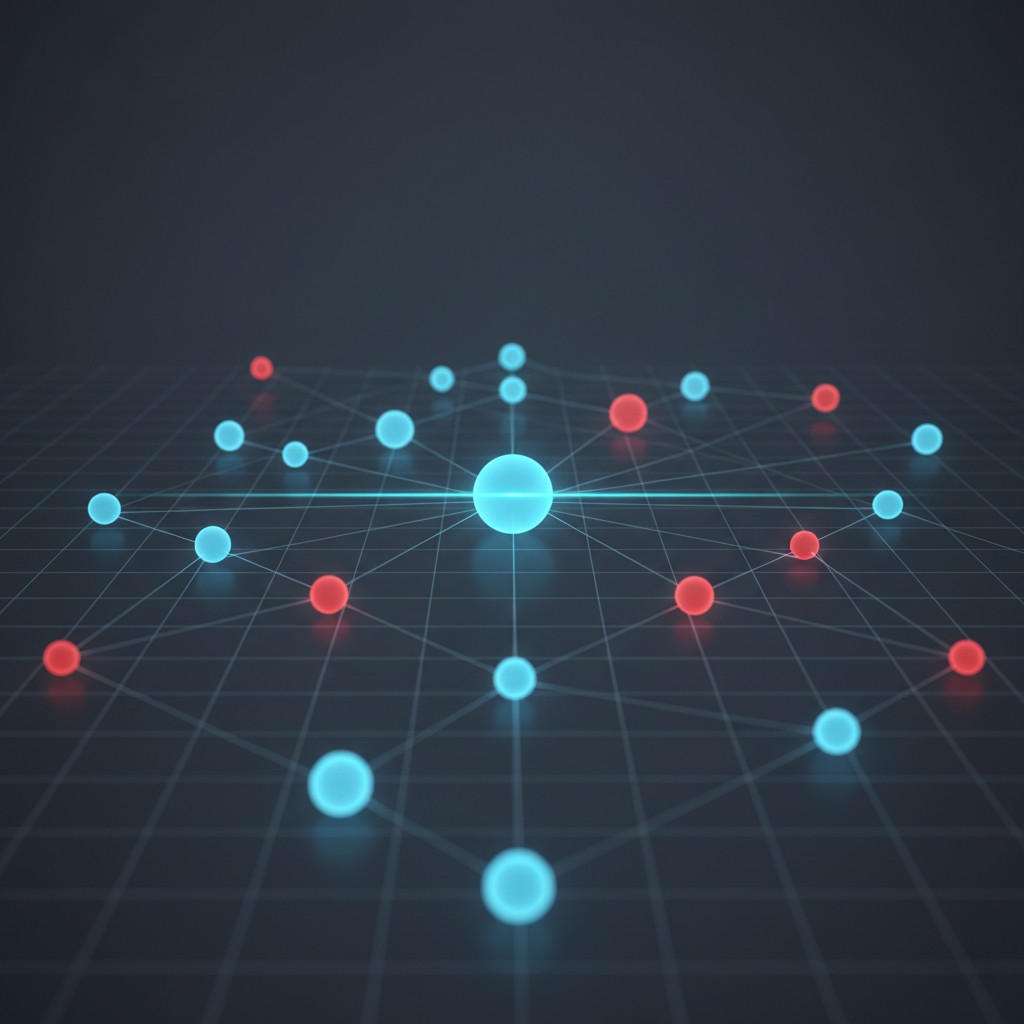

Systems define Social Scoring Integration as the inclusion of non-traditional relational data into risk modeling. This involves mapping the connectivity between high-risk profiles and emerging credit identities. When an agent maintains close digital ties with volatile profiles, the system may apply a risk premium. This process utilizes information asymmetry to fill gaps in traditional reporting. Consequently, the probabilistic evaluation layer adjusts the recovery slope based on these social graph variables.

Institutional models observe behavioral recurrence patterns within specific digital clusters. If a cluster demonstrates a collective trend toward deferred payments, the entire network faces increased structural friction. This logic assumes that individuals within a shared digital environment adopt similar consumption heuristics. Moreover, the system monitors the utilization velocity of social peers to predict an agent’s future liquidity state. This creates a multi-dimensional risk map that traditional scoring fails to capture.

Digital Associations and Systemic Friction

Proxy risks emerge when digital associations signal a departure from established stability baselines. Agents often underestimate the weight of “guilt by digital association” in 2026 audit frameworks. However, oversight mechanisms prioritize the integrity of the total network. When an agent enters a cluster characterized by cognitive tunneling, the system introduces defensive latency. This latency serves as a buffer against potential credit contagion within the social group.

The Federal Reserve Board has examined the implications of alternative data in credit decisioning. Modern models treat these social variables as secondary indicators of intertemporal stability. Profiles with “clean” social graphs—those associated with high-integrity clusters—receive friction reduction. In contrast, profiles linked to volatile nodes encounter a more restrictive modeling environment. As a result, maintaining a high-quality digital network becomes a structural necessity.

Behavioral Recurrence in Peer-to-Peer Environments

Utilization velocity often fluctuates based on peer-influenced consumption narratives. In the context of Social Scoring Integration, peer behavior acts as a leading indicator of individual default probability. Systems observe how agents respond to the credit reversion behavior of their closest digital neighbors. If the peer group fails to stabilize utilization, the individual profile is flagged for a modeled depreciation state. Therefore, the system preemptively limits exposure to prevent a localized relief trap.

Researchers utilize our Resources Hub to simulate how digital proximity impacts overall profile health. Understanding behavioral credit auditing shift 2026 is vital for navigating these invisible audit layers. Systemic mechanics favor profiles that demonstrate social independence from high-risk clusters. Maintaining a stable recovery slope requires active management of digital associations to avoid proxy-based downgrades.

This is a general educational framework, not personalized financial advice. We are not a credit bureau, lender, or scoring model provider.

The resilience of a credit identity depends on both individual discipline and collective association quality. Profiles aligned with stable digital networks maintain higher structural integrity over time. Recognizing the impact of social metadata is essential for modern profile optimization. These signals alert audit layers to potential hidden risks before they manifest in traditional data. As a result, agents who cultivate high-integrity associations secure a more robust statistical relationship with lending algorithms.

Research Abstract

This study explores Social Scoring Integration as an emergent risk-modeling frontier in 2026. By investigating ‘Network Contagion,’ the research identifies how digital proximity to volatile profiles creates systemic friction. The findings suggest that institutional audit layers increasingly rely on social graph metadata to predict individual solvency and behavior.

| Network State | Behavioral Indicator | Systemic Impact |

|---|---|---|

| High-Integrity Cluster | Associations with low-utilization profiles | Friction reduction; high reliability |

| Proximity Volatility | Digital ties to high-frequency BNPL users | Proxy Risk flag; defensive latency |

| Network Contagion | Cluster-wide default or late payment trends | Modeled depreciation; systemic restriction |

Data Accuracy Note (2026): Market conditions, Federal Reserve interest rates, and lender algorithms change rapidly. While we strive to provide the most accurate insights as of January 2026, we recommend verifying all specific loan terms and APRs directly with your chosen platform before signing any agreement.