Following our milestone research into The Halo Effect: Misjudging Profile Safety via Aesthetic Metrics, this 50th study examines Social Proof Bias within the 2026 credit architecture. As we reach this analytical midpoint, it is critical to understand how individual credit identities are influenced by collective behavior. In the current systemic landscape, oversight mechanisms prioritize the detection of “risk clusters.” Specifically, many borrowers adopt high-friction debt habits simply because their social or digital peers are doing the same. Consequently, this herd mentality creates pockets of systemic fragility that institutional algorithms monitor with extreme precision.

The Mechanics of Social Proof in Credit Clusters

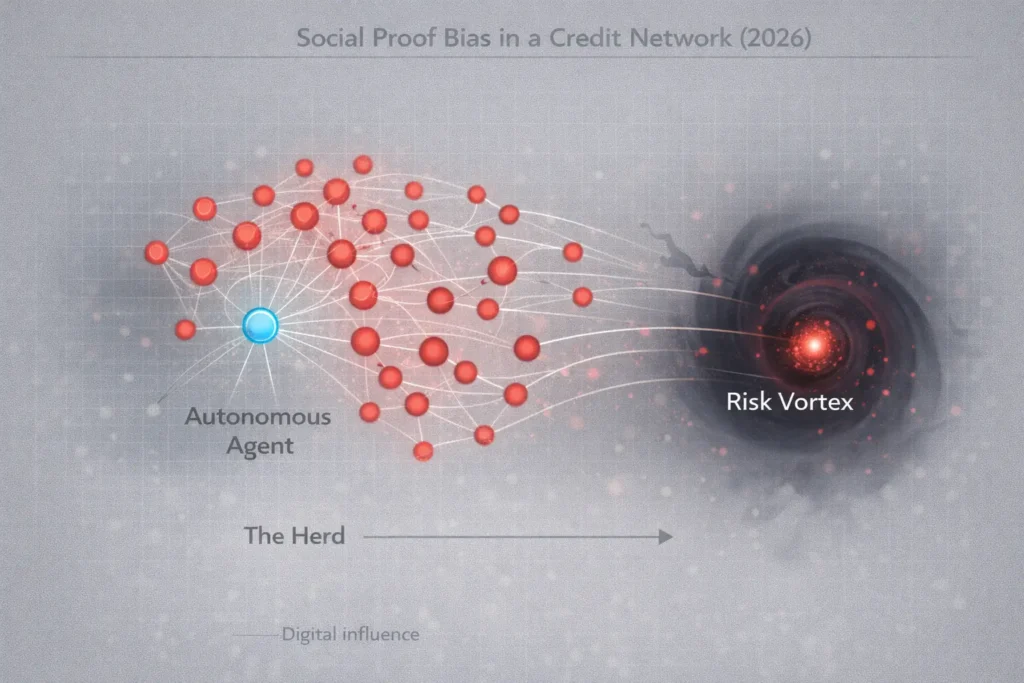

Systems define Social Proof Bias as a psychological phenomenon where people assume the actions of others in an attempt to reflect correct behavior for a given situation. Within 2026 audit layers, this manifests as “neighborhood risk contagion.” Notably, profiles that join peer-to-peer (P2P) lending circles or follow high-velocity “credit hacking” trends on social platforms trigger specific volatility markers. Indeed, the system views the adoption of popular but unverified financial strategies as a sign of cognitive dependency. Furthermore, the probabilistic evaluation layer increases friction when it detects that an agent’s utilization patterns mirror those of a high-risk social cluster.

Statistically, institutional data streams monitor the “behavioral correlation” between interconnected profiles. If a cluster of agents simultaneously adopts a specific “relief trap” strategy—such as rotating credit between high-interest apps—the model identifies a state of collective tunneling. Moreover, the system cross-references these shared patterns with historical default clusters. Subsequently, this analysis helps detect systemic “contagion” before it results in a localized collapse. Therefore, models may introduce mandatory “decoupling” friction for agents within these clusters. Specifically, these interventions ensure that the individual’s risk profile is insulated from the poor decisions of their peers.

Systemic Mechanics of Collective Contagion

Collective contagion serves as a primary behavioral filter for risk archetypes in 2026. Specifically, oversight mechanisms observe whether an agent can maintain an autonomous and objective financial strategy despite peer pressure. Conversely, profiles that demonstrate a “contrarian” stability—reducing utilization when their cluster is expanding—receive higher integrity scores. This suggests that the agent is free from the distorting effects of Social Proof Bias. Therefore, the audit layers prioritize these autonomous agents for friction reduction, as they prove a higher capacity for independent solvency management.

The World Economic Forum emphasizes that systemic resilience in 2026 depends on the mathematical decoupling of individual risk from social influence. In particular, modern models treat “socially-driven borrowing” as a leading indicator of repayment fragility. If an agent demonstrates a persistent pattern of following high-friction trends, it indicates a high level of information asymmetry and low temporal integrity. Consequently, the risk modeling environment becomes more restrictive for such profiles. As a result, the capacity for credit expansion remains limited until the agent proves they can navigate financial choices without relying on collective cues.

Strategic Friction as a Decoupling Tool

Strategic friction acts as a necessary corrective tool when Social Proof Bias threatens an agent’s structural health. When systems detect a profile is mirroring high-risk cluster behavior, they may initiate an “autonomy audit.” This intervention forces the agent to demonstrate their independent liquidity reserves and separate their liability trajectory from the group. Furthermore, systemic mechanics favor profiles that exhibit a self-correction trajectory after these forced disclosures. Specifically, this involves a measurable shift from “herd-based” spending to personalized, outcome-based settlement optimization.

In contrast, profiles that remain deeply embedded in high-risk social proof loops demonstrate lower temporal integrity. Managing the metadata associated with these collective traps requires an understanding of how behavioral credit auditing shift 2026 logic applies. Therefore, understanding these mechanics is essential for modern profile management. Researchers utilize our Resources Hub as an analytical modeling aid for these complex evaluations as we move into the next phase of our 2026 research series.

This is a general educational framework, not personalized financial advice. We are not a credit bureau, lender, or scoring model provider.

The resilience of a credit identity depends on maintaining cognitive independence from collective financial trends. Profiles that proactively decouple from high-risk clusters maintain higher structural integrity over time. Additionally, maintaining a stable trajectory requires recognizing that “popular” financial advice often leads to systemic friction. These signals alert the audit layers to potential groupthink and localized instability. As a result, agents who prioritize their own objective data over social proof secure a more robust statistical relationship with lending algorithms.

Research Abstract (Article 50 Milestone)

This milestone study investigates Social Proof Bias as a catalyst for systemic risk clusters in 2026. By analyzing the ‘Contagion of Bad Habits,’ the research identifies how algorithmic auditors detect peer-mirrored borrowing behavior. The findings suggest that ‘Behavioral Autonomy’—the ability to resist collective financial trends—is now a critical metric for maintaining a low-friction credit profile.

| Peer Interaction Level | Behavioral Marker | Systemic Risk Status |

|---|---|---|

| Autonomous Agent | Strategy independent of social trends | Friction Reduction; High Integrity |

| Cluster Mirror | Adopts P2P debt habits of social circle | Monitoring Alert; Stability Check |

| Trend Follower | High sensitivity to “credit hacking” social peaks | Modeled Depreciation; Defensive Decoupling |

Data Accuracy Note (2026): Market conditions, Federal Reserve interest rates, and lender algorithms change rapidly. While we strive to provide the most accurate insights as of January 2026, we recommend verifying all specific loan terms and APRs directly with your chosen platform before signing any agreement.