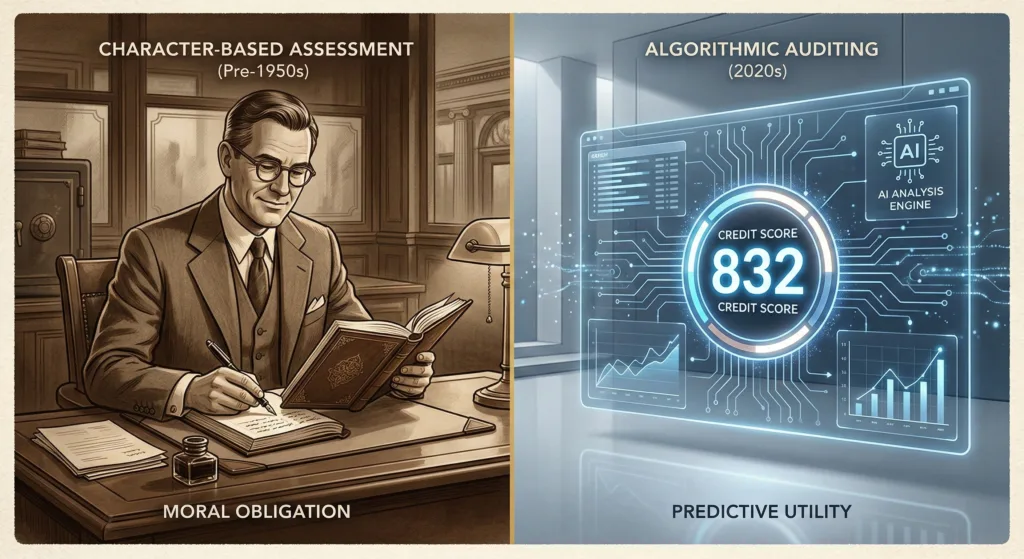

In the mid-20th century, obtaining a loan was not a matter of data; it was a matter of “character.” A local banker would look at your social standing, your family reputation, and your physical appearance to determine if you were creditworthy. This highly subjective, “Character-based” lending was the accepted norm until 1956, when an engineer named Bill Fair and a mathematician named Earl Isaac realized that human judgment was inherently biased and inefficient. Their collaboration birthed Fair, Isaac and Company (FICO), fundamentally altering the financial landscape.

Before the 1950s, credit evaluations relied heavily on the traditional “Three C’s”: Character, Capacity, and Capital. While these pillars remain conceptually relevant today, their measurement has shifted drastically from anecdotal evidence to rigorous statistical modeling. The original 1956 FICO model introduced a revolutionary concept: the “Credit Score”—a single, standardized numerical representation of a borrower’s probability of default.

This shift marked the world’s first true attempt at a “Systemic Audit.” By removing the local banker’s personal bias, the mathematical system allowed for the massive democratization of credit. However, it also introduced a new layer of friction: the impenetrable black box of algorithmic auditing.

As the use of automated credit scores exploded throughout the 1960s, so did critical errors in the data. Credit bureaus often operated in the shadows, and consumers had virtually no mechanisms to correct inaccuracies that could instantly ruin their financial lives. The passage of the Fair Credit Reporting Act (FCRA) in 1970 was a landmark moment for Financial Practice.

The FCRA established the foundational legal framework for data integrity. It legally mandated that if a mathematical system was going to judge a human being’s financial solvency, that system must be transparent, disputable, and accountable to the consumer. This era forced lenders to integrate rigorous data verification into their internal auditing processes, setting the stage for the modern systems we use today.

Today, we are navigating the third great evolution of credit assessment. We have transitioned from the manual, subjective reviews of the 1950s, through the rigid statistical models of the 1980s, to the dynamic, real-time AI auditing engines of 2026. Modern institutional lenders no longer just look at your past payment history; they analyze complex variables like your financial velocity and your systemic elasticity.

Understanding this historical evolution is crucial for any action-oriented user looking to optimize their profile through our Resources Hub. You are not just managing a three-digit number; you are navigating a 70-year-old evolving logic gate. To effectively master your credit profile today and survive algorithmic scrutiny, you must respect the mathematical foundation laid down decades ago.

| Historical Era | Primary Metric | Audit Method | Systemic Risk Focus |

|---|---|---|---|

| Pre-1950s | Character & Social Standing | Manual/Subjective Interview | Moral Obligation |

| 1950s – 1990s | Payment History (FICO) | Static Statistical Modeling | Historical Reliability |

| 2020s (Modern) | Behavioral & Real-time Data | Algorithmic/AI Auditing | Predictive Velocity |

Data Accuracy Note (2026): Market conditions, Federal Reserve interest rates, and lender algorithms change rapidly. While we strive to provide the most accurate insights as of January 2026, we recommend verifying all specific loan terms and APRs directly with your chosen platform before signing any agreement.