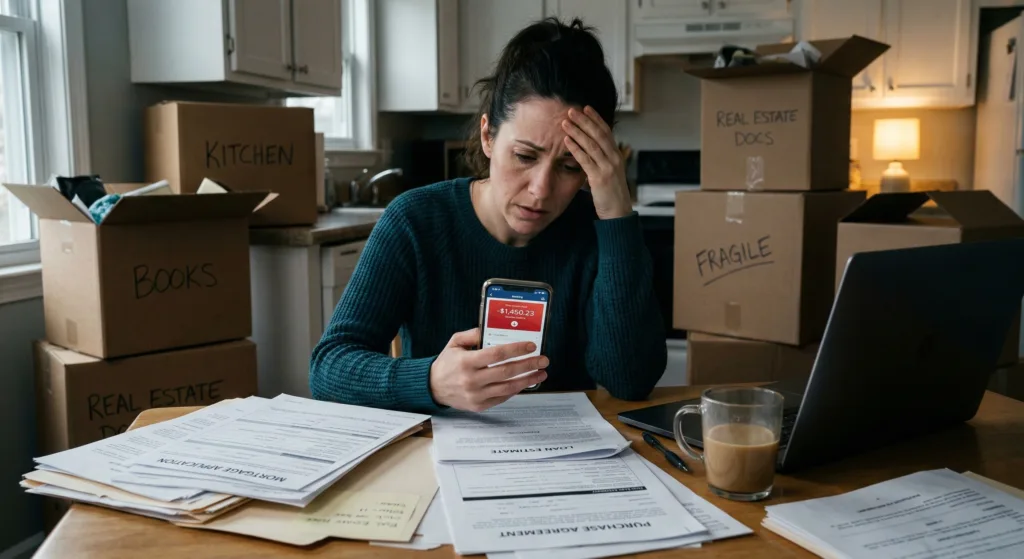

If you recently noticed a negative bank balance right before closing on a house, you might be panicking. The short answer is: a single $500 overdraft typically does not automatically ruin a mortgage application. However, it often triggers a red flag during your lender’s final soft pull. To protect your closing timeline, borrowers generally find it prudent to take two proactive steps: transferring funds to cure the negative balance immediately, and preparing a preemptive Letter of Explanation (LOE). Ignoring the issue can severely complicate the final underwriting process.

Educational Guide: Explaining a Recent Overdraft

*Educational example only. This sample is for informational purposes and does not represent financial, legal, or underwriting advice.

• 1 Recent Incident (within ~90 days): Often viewed as isolated; a brief explanation may be requested.

• Multiple Incidents (Pattern): May raise additional questions and could require further documentation.

Date: [Insert Date]

To: Underwriting Department

Re: Letter of Explanation for Overdraft on Account #[Last 4 Digits]

Dear Underwriter,

I am writing to explain the negative balance of -$[Amount] that occurred on [Date]. This was an isolated incident caused by [Brief factual reason, e.g., an auto-pay bill clearing before my paycheck deposit].

I transferred funds on [Date] to restore the balance. Attached is the updated transaction history reflecting the current status.

Sincerely,

[Your Name]

Institutional lenders monitor your accounts for signs of financial distress right up to the funding date. This intense scrutiny relates closely to the systemic risk metrics we analyzed in our deep dive on Debt-to-Income vs Debt-to-Equity ratios. Banks simply want to verify that your daily cash flow remains stable. For broader guidance on maintaining account health, you may also consult the CFPB resources on bank accounts.

Fictionalized Scenario: The Pre-Closing Panic

(Fictionalized persona for illustrative purposes only.)

Consider the case of David, a public school teacher scheduled to close on a home in 14 days. An unexpected $500 auto repair bill auto-drafted from his checking account, dropping his balance to -$120. His mortgage underwriter spotted this during the final verification of deposits. Because David panicked and waited three days to address the deficit, the underwriter temporarily suspended his clear-to-close status. He had to provide 60 additional days of bank statements to prove this was an isolated incident, which nearly jeopardized his locked interest rate.

The Veteran’s Audit Room Observation

Audit Room Observation: In my experience reviewing final funding conditions, an isolated overdraft is frequently viewed as an administrative error rather than a crisis. However, if the algorithm detects a pattern of Non-Sufficient Funds (NSF) fees over a 90-day period, the system may interpret this as systemic cash flow failure. The underwriter primarily wants to ensure you are not cannibalizing your mortgage reserves to pay for basic living expenses.

3 Actionable Steps to Protect Your Loan

If you face an overdraft during the underwriting process, you might consider these steps to help salvage your application:

- Cure the Deficit Quickly: Transfer funds from a verified, sourced account to bring the balance positive. Avoid depositing unverified mattress cash, as unexplained large deposits often create larger underwriting issues.

- Write a Preemptive Letter of Explanation (LOE): Do not wait for the underwriter to ask. Draft a simple, factual LOE stating the exact cause of the overdraft (e.g., “An annual insurance premium auto-renewed earlier than expected”).

- Provide the Updated Transaction History: Download an official transaction printout from your bank showing the cured balance and send it directly to your loan officer to help clear the algorithmic flag.

By handling the situation proactively, many borrowers successfully navigate this stressful hurdle and close on time.

Data Accuracy Note (2026): Market conditions, Federal Reserve interest rates, and lender algorithms change rapidly. While we strive to provide the most accurate insights as of January 2026, we recommend verifying all specific loan terms and APRs directly with your chosen platform before signing any agreement.